Volatility แปลว่าอะไร — ความผันผวนในตลาดการเงิน

Volatility

Volatility ความผันผวน Historical Implied VIX Standard Deviation ATR Bollinger Bands Option Pricing Risk Management Position Size Trading Strategy

| Volatility Type | Calculation | Timeframe | Use Case | Data Source |

|---|---|---|---|---|

| Historical (HV) | StdDev of Log Returns | Past 20-252 days | Risk assessment | Price history |

| Implied (IV) | Back-solved from Option | Forward looking | Option pricing | Option market |

| Realized | Actual StdDev period | Specific period | Performance eval | Price history |

| ATR | Avg True Range | 14 periods typical | Stop loss sizing | OHLC data |

| VIX | S&P 500 Option IV | 30-day forward | Market sentiment | CBOE |

| Bollinger BW | (Upper-Lower)/Middle | 20 periods | Squeeze detection | Price + StdDev |

เคล็ดลับ

- ATR: ใช้ ATR ตั้ง Stop Loss ให้เหมาะกับ Volatility ปัจจุบัน

- Size: ลด Position Size เมื่อ Volatility สูง

- Squeeze: สังเกต Bollinger Squeeze เตรียม Breakout Trade

- VIX: ดู VIX เป็น Sentiment Indicator ก่อนเทรด

- Regime: ปรับ Strategy ตาม Volatility Regime

การนำความรู้ไปประยุกต์ใช้งานจริง

แหล่งเรียนรู้ที่แนะนำ ได้แก่ Official Documentation ที่อัพเดทล่าสุดเสมอ Online Course จาก Coursera Udemy edX ช่อง YouTube คุณภาพทั้งไทยและอังกฤษ และ Community อย่าง Discord Reddit Stack Overflow ที่ช่วยแลกเปลี่ยนประสบการณ์กับนักพัฒนาทั่วโลก

อ่านเพิ่ม: Spark Structured Streaming CQRS Event Sourcing — วิธีตั้งค่า · อ่านเพิ่ม: Segment Routing Best Practices ที่ต้องรู้ | SiamCafe Blog · อ่านเพิ่ม: Seed Phrase | SiamCafe Blog

เนื้อหาเกี่ยวข้อง — อ่านต่อ: Mintlify Docs Capacity Planning —

เปรียบเทียบข้อดีและข้อเสีย

จากตารางเปรียบเทียบจะเห็นว่าข้อดีมีมากกว่าข้อเสียอย่างชัดเจน โดยเฉพาะในแง่ของประสิทธิภาพและความสามารถในการ Scale สำหรับข้อเสียส่วนใหญ่สามารถแก้ไขได้ด้วยการเรียนรู้อย่างเป็นระบบและวางแผนทรัพยากรให้เหมาะสม

แนะนำเพิ่มเติม — แหล่งความรู้ Forex iCafeForex

Volatility แปลว่าอะไร

ความผันผวน การเปลี่ยนแปลงราคา Standard Deviation สูงเปลี่ยนมาก ต่ำเปลี่ยนน้อย หุ้น Forex Crypto Option ความเสี่ยง โอกาส

เนื้อหาเกี่ยวข้อง — บทความที่เกี่ยวข้อง: หนังสือ demand supply zone

Historical กับ Implied Volatility ต่างกันอย่างไร

HV คำนวณจากอดีต StdDev Log Return IV คำนวณจาก Option ราคาตลาด อนาคต IV สูงกว่า HV ตลาดคาดผันผวนมาก Black-Scholes

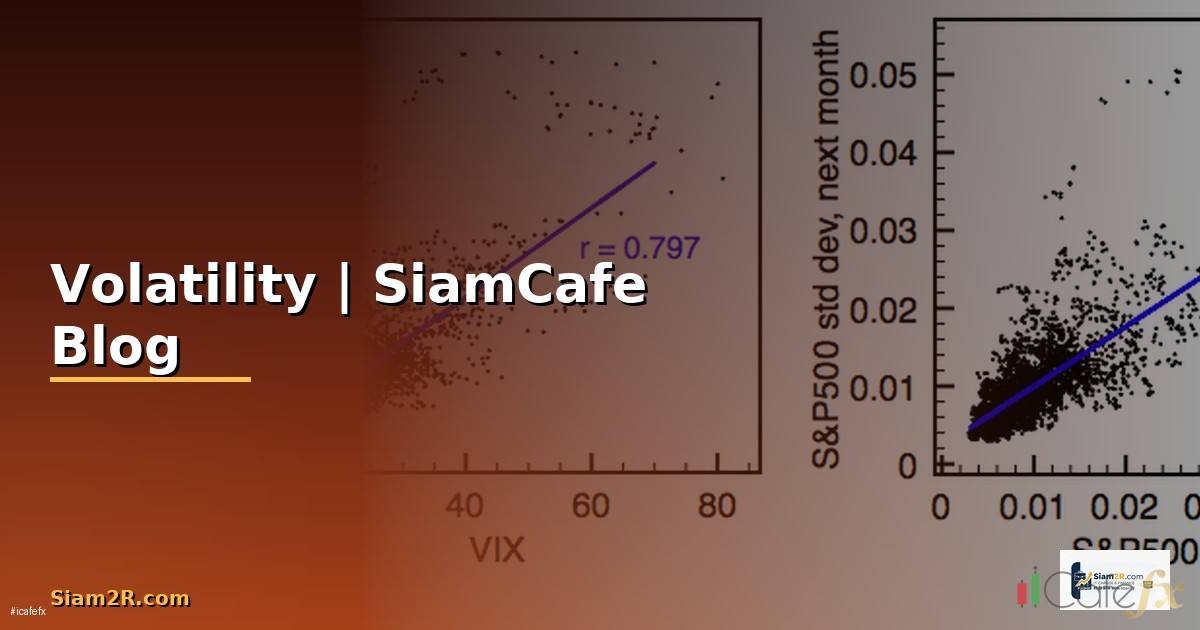

VIX Index คืออะไร

Volatility Index S&P 500 IV 30 วัน ต่ำกว่า 20 สงบ 20-30 ปานกลาง สูงกว่า 30 กลัว Fear Index ความเชื่อมั่น Futures ETF Options

แนะนำเพิ่มเติม — บทวิเคราะห์จาก XM Signal

เนื้อหาเกี่ยวข้อง — ทำความเข้าใจ Grafana Loki LogQL Micro-segmentation — คู่มือฉบับสมบูรณ์ 2026

ใช้ Volatility ในการเทรดอย่างไร

ATR Stop Loss Position Size Bollinger Bands Squeeze Breakout Mean Reversion VIX Sentiment Option Straddle Strangle Risk Reward Regime

สรุป

Volatility ความผันผวน Historical Implied VIX ATR Bollinger Bands Position Size Risk Management Regime Trading Strategy Option Pricing Production

เนื้อหาเกี่ยวข้อง — บทความที่เกี่ยวข้อง: Healthchecks.io Chaos Engineering —