Volatility คืออะไร — ทำความเข้าใจความผันผวนในตลาดการเงิน

Volatility ความผันผวน

Volatility ความผันผวน การเปลี่ยนแปลงราคาสินทรัพย์ วัดความเสี่ยง Historical Volatility Implied Volatility VIX Index Options หุ้น Forex Crypto

| ประเภท | วิธีวัด | ใช้ทำอะไร | ตัวอย่าง |

|---|---|---|---|

| Historical Vol | Standard Deviation ของ Returns | วัดความเสี่ยงในอดีต | HV 30 วัน |

| Implied Vol | คำนวณจากราคา Options | คาดการณ์อนาคต | IV ของ Options |

| Realized Vol | Actual Price Movement | เปรียบเทียบกับ IV | RV vs IV |

| VIX Index | IV ของ S&P 500 Options | วัดความกลัวตลาด | VIX > 30 = กลัว |

เคล็ดลับ

- HV vs IV: ถ้า IV > HV Options แพงเกินไป ขาย Premium

- VIX: VIX > 30 มักเป็นโอกาสซื้อ (Contrarian)

- Bollinger: Bandwidth แคบรอ Breakout ไม่เทรดใน Squeeze

- Position Size: Volatility สูง ลดขนาด Position ลง

- Diversify: ผสมสินทรัพย์ Low Vol + High Vol ลดความเสี่ยงรวม

การนำความรู้ไปประยุกต์ใช้งานจริง

แหล่งเรียนรู้ที่แนะนำ ได้แก่ Official Documentation ที่อัพเดทล่าสุดเสมอ Online Course จาก Coursera Udemy edX ช่อง YouTube คุณภาพทั้งไทยและอังกฤษ และ Community อย่าง Discord Reddit Stack Overflow ที่ช่วยแลกเปลี่ยนประสบการณ์กับนักพัฒนาทั่วโลก

เนื้อหาเกี่ยวข้อง — MQL4 Json — คู่มือเทรด Forex ฉบับสมบูรณ์ 2026 —

เปรียบเทียบข้อดีและข้อเสีย

| ข้อดี | ข้อเสีย |

|---|---|

| ประสิทธิภาพสูง ทำงานได้เร็วและแม่นยำ ลดเวลาทำงานซ้ำซ้อน | ต้องใช้เวลาเรียนรู้เบื้องต้นพอสมควร มี Learning Curve สูง |

| มี Community ขนาดใหญ่ มีคนช่วยเหลือและแหล่งเรียนรู้มากมาย | บางฟีเจอร์อาจยังไม่เสถียร หรือมีการเปลี่ยนแปลงบ่อยในเวอร์ชันใหม่ |

| รองรับ Integration กับเครื่องมือและบริการอื่นได้หลากหลาย | ต้นทุนอาจสูงสำหรับ Enterprise License หรือ Cloud Service |

| เป็น Open Source หรือมีเวอร์ชันฟรีให้เริ่มต้นใช้งาน | ต้องการ Hardware หรือ Infrastructure ที่เพียงพอ |

จากตารางเปรียบเทียบจะเห็นว่าข้อดีมีมากกว่าข้อเสียอย่างชัดเจน โดยเฉพาะในแง่ของประสิทธิภาพและความสามารถในการ Scale สำหรับข้อเสียส่วนใหญ่สามารถแก้ไขได้ด้วยการเรียนรู้อย่างเป็นระบบและวางแผนทรัพยากรให้เหมาะสม

Volatility คืออะไร

ความผันผวน การเปลี่ยนแปลงราคาสินทรัพย์ วัดความเสี่ยง Historical Implied VIX สูง=เสี่ยงมาก กำไร/ขาดทุนมาก

แนะนำเพิ่มเติม — ดูสัญญาณเทรดที่ XM Signal

เนื้อหาเกี่ยวข้อง — อ่านต่อ: XAU USD คืออะไร — อัตราแลกเปลี่ยนล่าสุด 2026 — คู่มือฉบับสมบูรณ์ 2026

Historical Volatility คำนวณอย่างไร

Standard Deviation ของ Daily Log Returns คูณ sqrt(252) Annualized HV 20% ราคาอาจเปลี่ยน 20% ใน 1 ปี

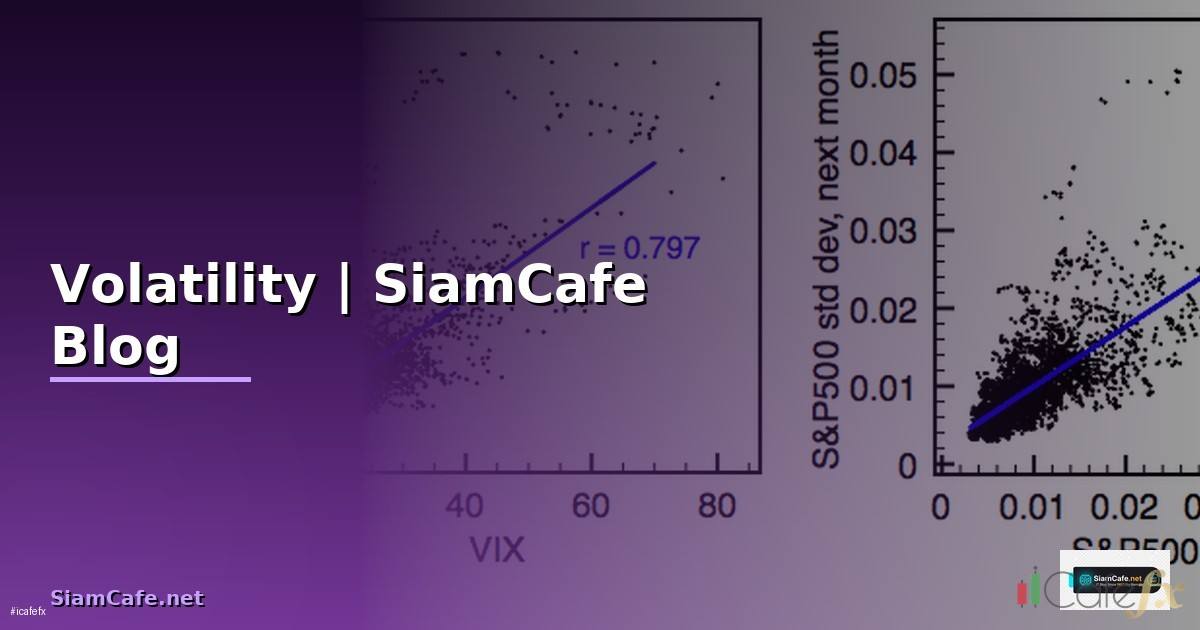

VIX Index คืออะไร

Volatility Index Fear Index S&P 500 Implied Volatility ต่ำกว่า 15 สงบ 25-35 ผันผวน มากกว่า 35 ตื่นตระหนัก

แนะนำเพิ่มเติม — หนังสือเทรดที่ SiamCafeBook

เนื้อหาเกี่ยวข้อง — ดูเพิ่มเติมเรื่อง Distributed Tracing Low Code No Code

Implied Volatility ใช้ทำอะไร

ตีราคา Options IV สูง Options แพง คาดการณ์ราคาอนาคต IV Crush หลัง Event ซื้อ IV ต่ำ ขาย IV สูง

สรุป

Volatility ความผันผวน Historical Implied VIX Fear Index Standard Deviation Returns Bollinger Bands Options Pricing IV Crush Position Sizing Risk Management Diversification

เนื้อหาเกี่ยวข้อง — ทำความเข้าใจ Bio — คู่มือฉบับสมบูรณ์ 2026

ทดลองเทรดฟรี XM — โบรกที่ อ.บอม ใช้เทรดจริง (พาร์ทเนอร์ XM)